CIBIL

CIBIL is the repository of information which is pooled in from all Banks and lending Institutions operating in India. The Credit Information Companies (Regulation) Act, 2005, and various Rules and Regulations issued by Reserve Bank of India has empowered CIBIL to collect the data from various types of lenders and then share the same within the group. The legislation has enabled banks to submit data to CIBIL. This has enabled CIBIL to tracks repayment history of bank customers loans, credit cards and further banking finances.

Punch In Your Details To Calculate Your Credit-Score

Personal Information*

For credit grantors to gain a complete picture of the payment history of a credit applicant, they must be able to gain access to the applicant's complete credit record that may be spread over different institutions. CIBIL collects company and consumer credit-related data and collates such data to create and distribute credit reports to Members.

CIBIL collects commercial and consumer credit-related data and collates such data to create and distribute credit reports to Members.(A Credit Information Report (CIR) is a factual record of a borrower's credit payment history compiled from information received from different credit grantors. Its purpose is to help credit grantors make informed lending decisions. CIBIL caters to both company and consumer segments. The Consumer Credit Bureau covers credit availed by individuals while the Company Credit Bureau covers credit availed by non-individuals such as partnership firms, proprietary concerns, private and public limited companies.

Today almost no loan or credit card application gets approved without checking the applicant's CIBIL report and CIBIL TransUnion Score.

CIBIL calculates an individual's credit score through advanced analytics and assigns a number between 300 and 900 to a borrower, based on his/her credit history. The closer your score to 900, the more confidence the credit institution will have in your ability to repay the loan and hence, the better the chances of your application getting approved. While each bank will have its own credit scoring cut-off based on the credit sanctioning policies, it has been observed that most banks are lending to consumers with a CIBIL TransUnion Score of 750 and above.

Credit information company has its own proprietary algorithm to calculate an individual's credit score, the most important elements of the score composition are centric around the loan payment behavior of the individual.

The score is calculated based on the following factors:

- Trade Attributes: How old are the consumer's lines of credit? What type of credit does the consumer have? Does the consumer have a good mix or balance of credit.

- Credit Utilization: Amount of credit is the consumer is using.

- Defaulting: How many accounts are past due and by how much time they are due.

Various factors that impact the CIBIL Transunion Score:

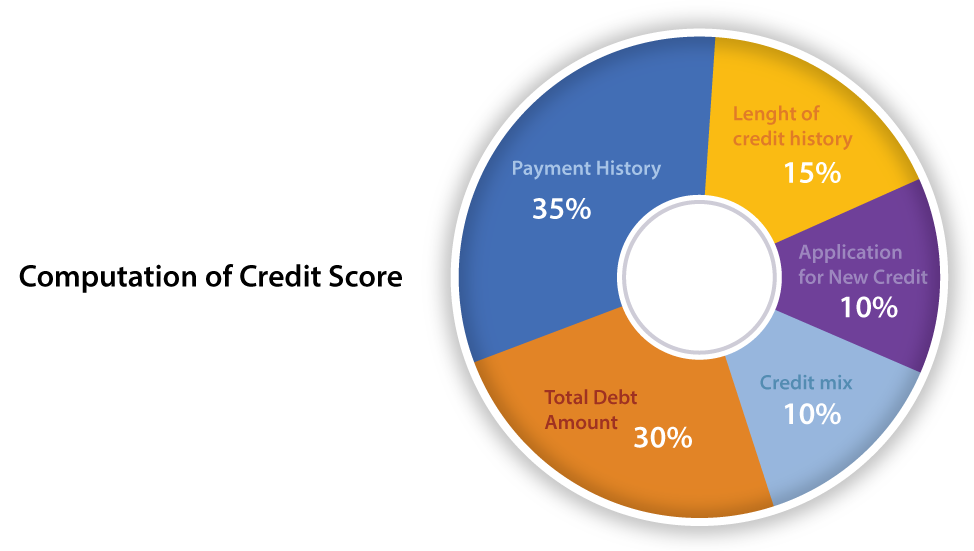

- Past Performance: Individuals past performance on their debt obligations is the most important criterion and contributes approximately 30% weightage to the score.

- Credit Exposure: The total amount of credit exposure contributes another 25% to the score.

- Credit Type & Duration: Type of loan availed whether secured or unsecured loan, and the duration of credit history established contributes 25% to the score.

- Other factors: Other factors such as credit utilization, recent credit behavior contribute the remaining 20% to the score.

CIBIL Report and CIBIL TransUnion Score not only determine whether or not you qualify for a loan, but it may also have an impact on the terms and conditions on which you can avail the loan. The higher the credit score, the better your chances of availing the loan faster and on favorable terms. It is advisable to check your CIBIL Report and CIBIL TransUnion Score before applying for a loan. Timely payments of loan EMIs is most important for maintaining a good credit history and a healthy credit score.

As CIBIL plays the role of the prime factor for your loan approval, it is very important in your financial journey.

- Interest Rates: For getting best interest rates and terms, you are required to obtain a decent CIBIL score. A good CIBIL score will help in saving money with lower interest rates for your loans.

- Credit Approvals: Your eligibility for obtaining the loan will be determined by the CIBIL score. A worse CIBIL score will decrease the chances of obtaining the loan without hassles. So for obtaining mortgage loan, car loan, personal loan, credit card or home loan, or any type of loan, a proper CIBIL score is required.

A CIBIL report plays a prominent role in an individual’s financial journey. The lenders depend on your CIBIL report to verify an individual’s creditworthiness. The main purpose of a CIBIL Report is that it aids the lender as well as the borrower in identifying and understanding their credit history clearly and completely.

- Purpose of a CIBIL Report: A CIBIL Report helps to measure the ability of a borrower to repay the loan. The lenders refer to the report and measure how much loan an individual currently has and if any loan can be taken further.

- Decides the credibility: CIBIL Report describes the credibility of an individual.

- Maintains a Monthly Record: CIBIL Report is based is based on the month on month details about the type of loans and the number of loans taken by an individual/company. It provides the entire credit related information of an individual/company.

- Helps for Further Improvement: The CIBIL Report facilitates an individual to analyze the complete credit history and understand the scope of improvement in different areas.

Credit scoring is a complex calculation, and the more you know about how credit reports and credit scores work, the better you can take control of your own credit. In addition to knowing the most important factors considered in credit scoring, it can be helpful to know a few other facts about credit reports and credit scores.

These are a few things that tend to be most important:

- Negative information on your credit report can lower your credit scores. That information remains on your credit report for a set period of time. For example, late payments appear for seven years from the date you first missed a payment. Paying off a collection account won’t remove it from your credit report. Bankruptcies can remain on your report for seven to ten years, depending on the type of bankruptcy. The good news is, all negative information will eventually cycle off your credit report. Until it does, focus on the things you can positively influence, including paying all your bills on time.

- You don’t need to carry a monthly credit card balance in order to build your credit history. You can pay off your credit card bills every month and positively affect your credit standing.

- Settling accounts for less than the full amount you owe can harm your credit score. Any time you fail to repay a debt as you originally agreed, it can negatively affect your credit. That said, the negative impact of settlement is still less than the negative effect of not paying a debt at all or declaring bankruptcy.

About

Services

Contact

Office No. 2, First Street Floor, Shruti House, Kelkar Road, 143, Narayan Peth, Pune, Maharashtra-411030.